Life Insurance

Financial protection for the people who matter most.

Life insurance is more than a policy; it’s a promise that your family will be okay.

Whether it’s $50,000 to cover final expenses or $500,000 to pay off a mortgage, we help you find the right fit without the frustration.

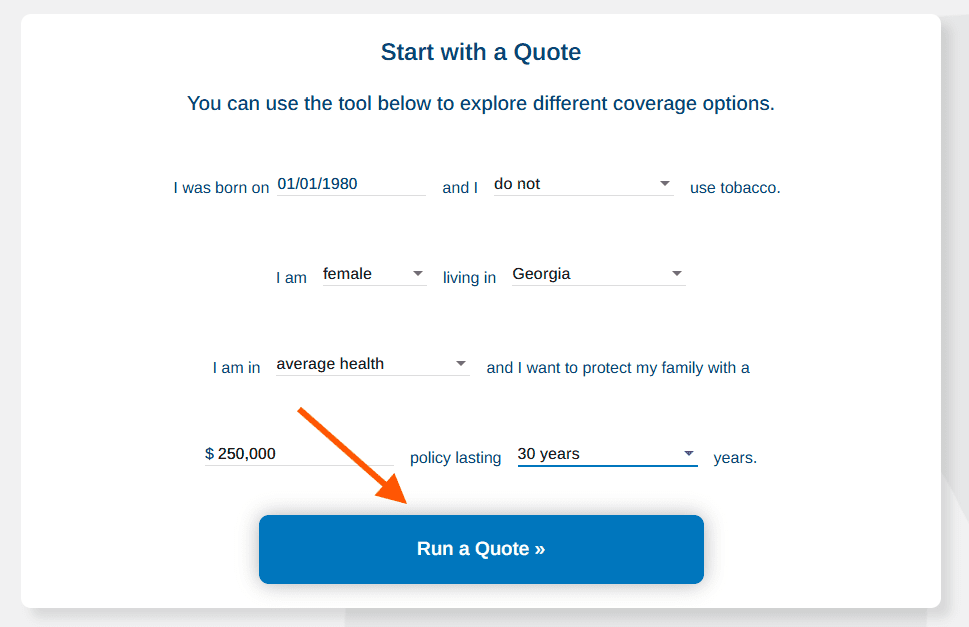

Quick Quote

Use our free quoting tool to get an instant quote on term life insurance.

Note: Excessive shopping for life insurance can work against you. Speak to us first. We help you navigate your options before you apply.

How Much Does Life Insurance Cost?

The cost of life insurance varies greatly based on several factors:

- Age and Health: Younger, healthier individuals generally pay lower premiums.

- Coverage Amount: Higher death benefits result in higher premiums.

- Policy Type: Term life insurance is typically more affordable than whole or universal life.

- Lifestyle and Occupation: High-risk activities or dangerous jobs can increase premiums.

- Insurance Company: Different companies have varying underwriting standards and pricing structures.

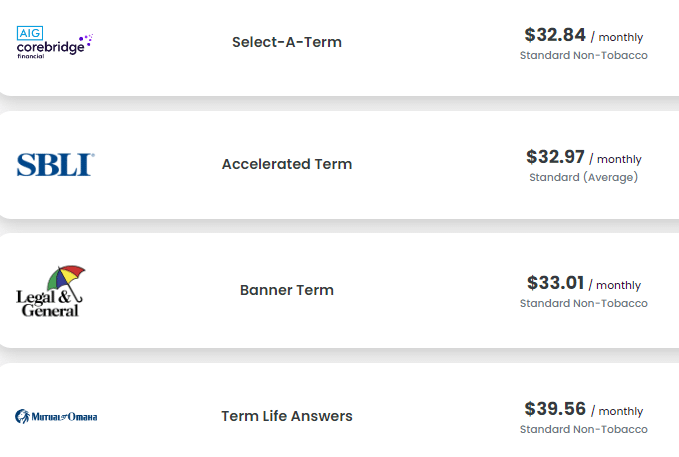

Take a look at the following examples for term life insurance:

#1) Term Life – Male, nonsmoker, fair health, age 30

- $250,000 policy

- 30-year term

For illustration only. Plans & price will vary. Contact us for a personalized quote.

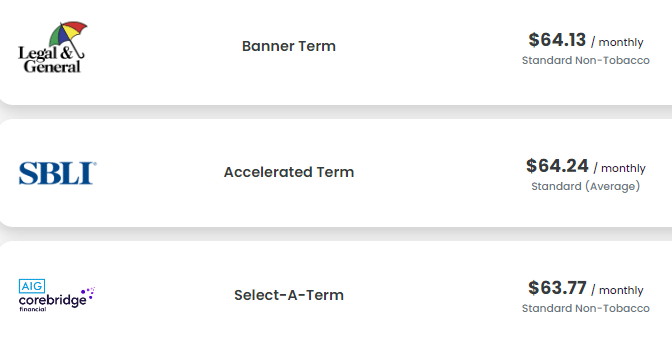

#2) Term Life – Female, nonsmoker, average health, age 40

- $500,000 policy

- 25-year term

For illustration only. Plans & price will vary. Contact us for a personalized quote.

No Medical Exam? How It Works

Many of our clients qualify for Instant Term Life.

This streamlined process uses your digital records (prescription history, MIB file, and motor vehicle reports) to provide an approval in minutes rather than months.

- Guaranteed Issue: For those with more severe health challenges, we offer options that require no health questions at all.

- Accelerated Underwriting: A middle ground that offers higher coverage amounts than “Instant” plans but still bypasses the traditional medical exam for qualified applicants.

No-medical exam life insurance may be convenient, but it often comes with limitations:

- Higher Premiums: You’ll likely pay significantly more than for a policy requiring a medical exam.

- Lower Coverage Limits: Coverage amounts are usually capped, and you may not qualify for large policies.

- Limited Eligibility: You might not qualify if you have certain health conditions or are significantly overweight.

Life Insurance for Diabetics

Diabetes can affect your eligibility for life insurance and the cost of premiums.

Insurance companies have diverse criteria, so it’s best to be informed before contacting multiple insurers, as excessive inquiries can potentially harm your MIB Consumer Report.

Consider these underwriting options when seeking life insurance with diabetes:

Accelerated Underwriting: This option involves a more in-depth review of your medical history but may offer higher coverage amounts and more flexible underwriting guidelines.

Simplified Issue: This option requires less medical information and can be faster, but it may have lower coverage limits and higher premiums.

Guaranteed Issue: This option provides coverage regardless of your health, but it typically has higher premiums and limited coverage amounts.

If you have a health condition like diabetes or high blood pressure, you still have options for life insurance.

Simplified or accelerated underwriting can help you secure coverage.

Get free expert guidance. Schedule a phone consultation with a licensed agent at your convenience.

Get A Quote

We make it easy for individuals, families & small business owners to find affordable coverage and peace of mind.

Start an instant quote and enroll online!

Ted McNeil

Owner, Broker

BenZen Insurance

An Independent Agency