Finding term life insurance with type 2 diabetes can seem daunting, but it’s absolutely achievable!

This guide provides practical tips and insights to help you navigate the application process and secure the coverage you need.

While having type 2 diabetes is a factor, it doesn’t automatically disqualify you from getting life insurance.

Understanding the process and taking proactive steps can greatly increase your chances of approval.

Knowing what to expect and how to approach the process can significantly improve your chances of getting approved for life insurance as a type 2 diabetic.

As an independent agency, we have firsthand experience with the challenges of diabetes and are committed to helping you find the coverage you deserve.

We’ll help you get life insurance with type 2 diabetes:

- Free Expert Guidance: We provide free expert guidance, pre-qualifying your application and working with you to optimize it, maximizing your chances of securing the coverage you deserve. We are compensated by the carrier for the support we provide so there’s no charge to you!

- Specialized Carriers: We partner with top-rated life insurance providers that specialize in offering coverage for chronic conditions like type 2 diabetes and high blood pressure, ensuring you get the best possible rates and terms.

- Compassionate Support: Our agents understand the challenges of living with diabetes. Many have personal experience with the condition, offering truly compassionate and informed guidance.

- Privacy & Confidentiality: Your privacy is our priority. We never share your personal details or ask for payment information, ensuring a safe transaction.

- Easy Online Application: Apply quickly and easily online, with expert support available every step of the way.

Tip: Speak to a licensed expert before you apply to save time, money & frustration. And avoid excessive “shopping.” More on that below.

By working with an experienced broker and managing your diabetes effectively, you can increase your chances of securing the best life insurance rates and terms.

Life Insurance Options for Type 2 Diabetics

Getting life insurance with diabetes requires careful consideration.

While term life, whole life and universal life insurance are common options, navigating the application process with a pre-existing condition can be tricky.

One size does not fit all and the choice depends on your financial goals, risk tolerance, and the specifics of your diabetes management.

Here’s a simplified view to help you understand the key differences:

Term Life

- Typically the most affordable option.

- Offers a relatively straightforward application process.

- Provides coverage for a specific term (e.g., 10, 20, or 30 years).

- Underwriting primarily focuses on your current diabetes management and overall health.

Whole Life

- Generally more expensive than term life.

- Provides lifelong coverage.

- Builds cash value over time.

- Involves a more complex application and stricter underwriting.

- Insurers assess long-term diabetes-related risks.

Universal Life

- Offers flexible premiums and death benefits.

- Builds cash value that can be used to adjust premiums.

- Underwriting is usually more involved than term, but less involved than whole.

- Like whole life, insurers will look at long-term risks.

For this article, we’ll focus on term life insurance for diabetics as it is often the most accessible and cost-effective choice.

How Term Life Insurance for Type 2 Diabetics Works

Living with type 2 diabetes presents unique challenges, especially when it comes to obtaining life insurance.

You might worry that diabetes will automatically lead to sky-high premiums or even denial of coverage.

Insurance companies assess risk when determining premiums, and type 2 diabetes, or a health condition like high blood pressure, is considered a risk factor.

Underwriting is the most critical step in obtaining life insurance for diabetics.

- A1C Levels: This blood test measures your average blood sugar over the past 2-3 months and is a key indicator of diabetes control. Lower A1C levels generally translate to more favorable best term life insurance rates Type 2 Diabetes.

- Medication: The type and dosage of medication you’re prescribed play a role. Well-managed diabetes with oral medication often presents less risk than insulin dependence, impacting your best term life insurance rates Type 2 Diabetes.

- Complications: Any diabetes-related complications, such as neuropathy, retinopathy, or cardiovascular issues, will be taken into consideration when determining your best term life insurance rates Type 2 Diabetes.

- Overall Health: Your overall health, including weight, blood pressure, and other medical conditions, also influence the best term life insurance rates Type 2 Diabetes you can qualify for.

- Family History: A family history of diabetes-related complications may be considered when calculating best term life insurance rates Type 2 Diabetes.

While A1C, BMI and other factors can impact your life insurance options, it doesn’t automatically disqualify you.

Contact us for assistance!

Where to Get Term Life Insurance for Type 2 Diabetics

Despite the challenges, getting affordable term life insurance with type 2 diabetes is entirely possible.

Before you apply for term life insurance as a diabetic be prepared to answer these prequalifying questions:

- Do you take insulin?

- What is your most recent A1C test value?

- How long have you had diabetes?

- What is your current age, height & weight

Foresters Financial

- Diabetes-Friendly Programs: Offers specialized programs designed for individuals with type 1 and type 2 diabetes.

- Simplified Underwriting: Quick and easy application process with fewer medical requirements.

- Exclusive Member Benefits: Access to discounted diabetes management products.

Banner Life (Legal & General)

- Flexible Underwriting: Considers individual health profiles and may offer more favorable terms for well-managed diabetes.

- Competitive Rates: Potential for affordable coverage with good health history.

Mutual of Omaha

- Established Reputation: Known for reliable coverage and customer service.

- Tailored Plans: Offers a range of life insurance options to suit various needs and budgets.

Additional Tips:

- Work with an Insurance Agent: An experienced agent can help you navigate the complexities of life insurance for diabetics and find the best options for your specific needs.

- Avoid Excessive Shopping: Get free quotes from multiple insurers to ensure you get the best possible deal, but try to avoid applying excessively (see below)

- Maintain a Healthy Lifestyle: Prioritize regular exercise, a balanced diet, and consistent medication adherence to improve your overall health and insurance eligibility.

If you have diabetes and are concerned about getting approved for life insurance, we can help.

Types of Life Insurance for Type 2 Diabetics

Different types of underwriting refer to the varying levels of medical scrutiny and information required to assess an applicant’s risk.

This can differ significantly depending on the insurer you choose.

Understanding these differences upfront can save you a lot of time and effort.

Underwriting Life Insurance for Type 2 Diabetics

When a diabetic applies for life insurance several key factors can influence the decision :

- Severity of Diabetes: The severity of your diabetes, as measured by factors like A1C levels and the presence of complications, can significantly impact your risk profile and, consequently, your premiums

- Diabetes Management: How well you manage your diabetes, including your adherence to treatment plans, diet, and exercise, can influence your eligibility and the cost of premiums

- Duration of Diabetes: The length of time you have had diabetes can be a factor. Longer durations may increase your risk

- Comorbidities: If you have other health conditions in addition to diabetes, such as heart disease, high blood pressure, or obesity, your risk may be higher.

- Lifestyle Factors: Your lifestyle habits, including smoking, excessive alcohol consumption, or dangerous hobbies, can also influence your eligibility and premiums

- Age: Your age is a significant factor affecting premiums. Diabetics over 50 generally have higher premiums

- Weight: Excess weight can exacerbate diabetes and increase your overall health risks, potentially leading to higher premiums

- Coverage Amount: The amount of coverage you seek can also impact your premiums. Larger coverage amounts may require more stringent underwriting

Traditional Life Insurance Underwriting

With a traditional life insurance application, the underwriter typically requires:

- Medical exam: This may include physical examination, blood tests, and other assessments.

- Lab work: Blood tests to evaluate your overall health and identify any underlying conditions.

- Medical records: Documentation of your medical history, including previous diagnoses, treatments, and hospitalizations.

These plans are generally best suited for healthy individuals who want the lowest premiums and are willing to go through a more in-depth review process.

Accelerated Underwriting vs. Simplified Issue

Two underwriting options that may be more favorable for individuals with diabetes are accelerated underwriting and simplified issue.

- Accelerated Underwriting: This involves an in-depth review of your medical history, but often with no medical exam. Offers more flexible underwriting guidelines with higher policy limits.

Best for healthy individuals looking for a fast approval process without a medical exam.

- Simplified Issue: This option requires less medical information and can be faster, but it may have lower coverage limits and higher premiums. It’s suitable for individuals with relatively stable health and well-controlled diabetes.

Best for applicants who may have minor health concerns but still want convenient, affordable coverage.

Tip: Avoid Excessive “Shopping”

While it’s essential to shop around to find the best rates and coverage, applying excessively can have unintended consequences.

The Medical Information Bureau (MIB) is a non-profit organization that collects and shares medical information about individuals who apply for life insurance.

When you apply for life insurance, your information is reported to the MIB.

Excessive shopping can lead to multiple inquiries on your MIB report, which may raise red flags for insurers. This could result in higher premiums or even denials.

- Limit inquiries: Try to keep the number of applications you submit within a reasonable timeframe.

- Be honest and accurate: Provide truthful information on all applications. Assume the insurance company can verify your answers!

- Consider pre-qualification: Some insurers offer pre-qualification options that allow you to assess your eligibility without affecting your MIB report.

- Work with an insurance agent: A knowledgeable agent can help you navigate the insurance market and find suitable options without excessive shopping.

Honesty is the Best Policy

It’s crucial to be honest about your diabetes on your life insurance application. Withholding information can lead to policy denial or, worse, a denied claim in the event of death.

By being upfront about your condition, you can work with the insurer to find the best coverage options.

Not to mention insurance companies use a variety of data sources like MIB to verify your health and financial information so it’s best to disclose everything upfront!

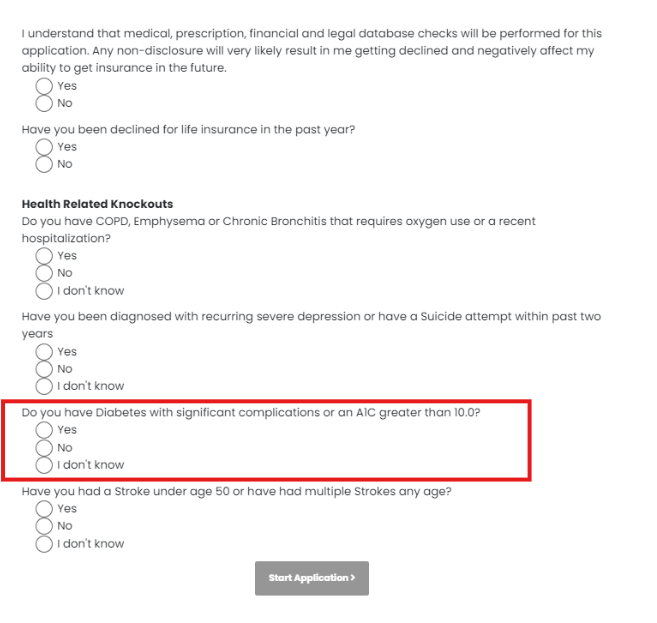

Sample Life Insurance Application Questions

The Cost of Term Life Insurance for Type 2 Diabetics

The cost of life insurance for diabetics can vary significantly. However, you may be able to find affordable options by shopping around and comparing quotes from different companies.

- Work with a Knowledgeable Agent: An experienced agent can help you navigate the process and find the best policy for your needs.

- Maintain a Healthy Lifestyle: A healthy lifestyle can improve your overall health and potentially lower your premiums.

- Consider Simplified Issue: These policies may have less stringent underwriting requirements, making them easier to qualify for.

By understanding the factors that influence life insurance rates for diabetics and taking proactive steps, you can secure affordable coverage that provides financial protection for your loved ones.

For illustration only. Your rates will vary:

Example 1 – Male, nonsmoker, age 40

- 30-year term life, $100,000

- no insulin

- A1C = 9.0

- duration = 5 years

- height = 5′ 10″

- weight = 250

Premium: $40-$50 a month

Example 2 – Female, nonsmoker, age 35

- 30-year term life, $200,000

- insulin

- A1C = 8.0

- duration = 10 years

- height = 5′ 6″

- weight = 180

Premium: $80-$95 a month

Example 3 – Male, nonsmoker, age 50

- 20-year term life, $300,000

- no insulin

- A1C = 7.5

- duration = 5 years

- height = 5′ 10″

- weight = 200

Premium: $150-$200 a month

Get free expert guidance before you apply for life insurance. Contact us or schedule a phone consultation with a licensed agent Monday-Friday with no obligation!

Tips to Get Life Insurance for Type 2 Diabetics

Here’s how to improve your chances of finding the best term life insurance rates type 2 diabetes:

Look for “Guaranteed Issue” or “Simplified Issue” Policies (with caution)

These policies have relaxed underwriting requirements but usually come with higher premiums and lower coverage amounts.

They should be considered as a last resort when seeking best term life insurance rates type 2 diabetes.

Work with an Independent Broker

Independent brokers have access to multiple insurance companies and can shop around to find the best rates for your specific situation.

They understand the nuances of underwriting for individuals with diabetes and can match you with insurers that are more lenient, helping you find the best term life insurance rates type 2 diabetes.

Be Proactive About Your Health

Managing your diabetes diligently is the most important factor in securing favorable best term life insurance rates type 2 diabetes.

Maintain a healthy weight, follow your doctor’s recommendations, and keep your A1C levels in check. Documenting your efforts can be beneficial during the application process.

Compare Quotes from Multiple Insurers

Don’t settle for the first quote you receive. Different insurance companies have different underwriting guidelines.

Comparing quotes from several insurers specializing in insuring individuals with health conditions is crucial for finding the best term life insurance rates type 2 diabetes.

Consider a No-Medical-Exam Policy

While these policies might have slightly higher premiums, they can be an option if you’re concerned about the medical exam process or have difficulty getting traditional coverage.

However, they typically offer lower coverage amounts and may not offer the best term life insurance rates type 2 diabetes.

Be Honest and Transparent

Provide accurate and complete information on your application.

Withholding information can lead to denial of coverage or policy cancellation, impacting your ability to secure best term life insurance rates type 2 diabetes in the future.

Denied Life Insurance Because of Diabetes?

If you’ve been denied life insurance due to diabetes, consider waiting a year or two before reapplying.

During this time, focus on addressing any underlying health issues that may be contributing to your risk profile.

- Improve Your A1C: If your A1C is high, work with your doctor to improve your blood sugar control. This can significantly enhance your insurability and potentially lower your premiums.

- Weight Management: Strive for a healthy BMI through a balanced diet and exercise. A healthy weight can significantly improve your overall health and reduce your risk of complications

- Medication: Adhere to your prescribed medication regimen and consult with your healthcare provider regularly to ensure optimal treatment

- Cholesterol Control: Maintain healthy cholesterol levels to reduce your risk of heart disease, a common complication of diabetes

- Blood Pressure Management: Keep your blood pressure under control. High blood pressure can increase your risk of diabetes-related complications

Steps You Can Take

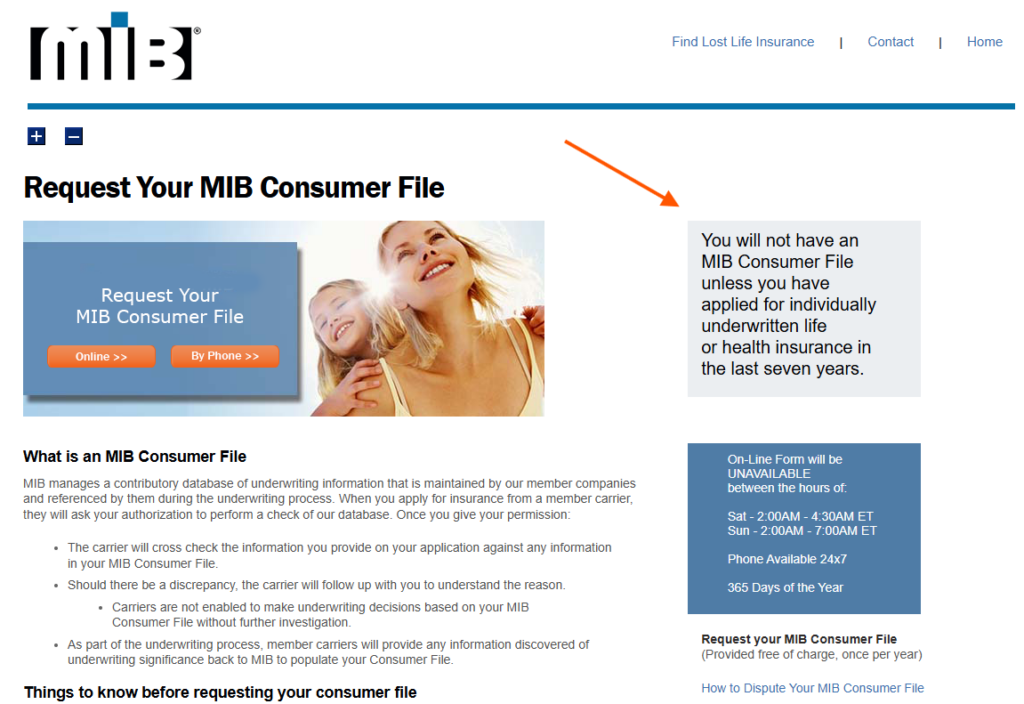

- Get a copy of your MIB Consumer File – If you’ve applied for life or disability insurance within the last 7 years you should have a file at MIB.

The MIB consumer report (similar to a credit report) contains much of the information insurance companies use to verify your information. It may contain your health history, medications and the results of your previous applications.

Note: Insurance companies know if you’ve applied elsewhere. Be consistent with your answers! - Employers often offer group life insurance with discounted premiums. Check with your employer to determine if a group policy is available. For the most part, your health is not a factor.

- Guaranteed-issue whole life insurance is a type of life insurance that doesn’t require you to undergo a medical exam or complete a health questionnaire.

It’s often the recommended life insurance for serious health conditions, patients and others when they don’t qualify for traditional life insurance.

Contact Us

We hope this post has provided insight as to what medical conditions can disqualify or deny you from life insurance.

During your search, there may be a time when consulting with an agent becomes necessary.

Life insurance depends on many risk factors like health, finances, credit score, lifestyle and even your driving record.

If you have questions contact us before you dive into an application.

There is no cost or obligation and it can save you time, money and the possibility of being denied coverage!

Licensed: FL, GA, MD, NC, NJ, PA, SC, TN, TX, VA

Information is meant to be accurate and educational and not intended to be legal, medical or financial advice. Do your own research and contact a professional for help. We earn revenue from partners & advertisers. Read our disclosure for more.

Owner, BenZen Insurance. Licensed insurance broker making it easy for individuals, families and business owners to get affordable health benefits.

His background in marketing, research, insurance, and financial services gives him a unique perspective to help others plan for a secure future and improve their physical, mental, and overall well-being.