We made it easy to find health insurance in Georgia for self-employed professionals.

Being your own boss offers lots of benefits, but also means taking on the responsibility of your own health coverage and possibly for your family too.

This guide was written for self-employed professionals, by self-employed professionals.

Our team specializes in helping sole proprietors, entrepreneurs and small business owners get affordable benefits in Georgia.

We’ll help you find the best health insurance in GA if you’re self-employed and answer questions like:

- How do self-employed individuals get health insurance?

- When can I apply for self-employed health insurance in GA?

- What’s the best health insurance for self-employed?

Free Assistance

As a Georgia Access Certified Broker, my team can help you find the best coverage for your needs and budget.

Same plans & prices with free dedicated support. That’s BenZen.

Ted McNeil

Owner, Broker

BenZen Insurance

Questions? Schedule your free consultation!

How to Get Health Insurance for Self-Employed in Georgia

The IRS defines self-employed as operating a business as a sole proprietor, independent contractor, or partnership with no employees.

You’ll want to look for individual coverage, not a group health plan.

When shopping for self-employed health insurance, it’s essential to understand the difference between a Qualified Health Plan (QHP) and short-term health insurance.

QHPs, available through the Health Insurance Marketplace, meet the coverage standards set by the Affordable Care Act (ACA), including essential health benefits and protections for pre-existing conditions.

Short-term health insurance is not available through the Health Insurance Marketplace and does not conform to Affordable Care Act (ACA) guidelines.

When Can I Apply for Health Insurance in Georgia for Self-Employed?

There are generally two main times you can enroll in health insurance in Georgia.

The first is during the Open Enrollment Period, which usually occurs annually between November 1st and January 15th.

This period allows most individuals, including the self-employed, to enroll without needing a specific reason.

Outside of Open Enrollment, you need to qualify for a Special Enrollment Period (SEP).

This is triggered by a Qualifying Life Event (QLE).

You typically have 60 days from the date of the qualifying life event to choose a new health plan.

Some common examples include:

- Losing existing health coverage, whether from an employer, Medicaid, or CHIP.

- Experiencing changes in your household, such as getting married, having or adopting a child, or getting divorced.

- Moving to a new state or a different health insurance service area within Georgia.

- Other specific situations like gaining U.S. citizenship or being released from incarceration.

For self-employed individuals, a change of income can qualify as a QLE, but you may need to show proof of prior coverage.

Ready to get started? Schedule your free consultation!

Georgia Health Insurance Marketplace

Georgia Access, the state based exchange replacing Healthcare.gov is the primary source of health insurance for self-employed in Georgia

Some may also refer to this as individual medical insurance.

Financial assistance may be available based on income, making coverage more affordable.

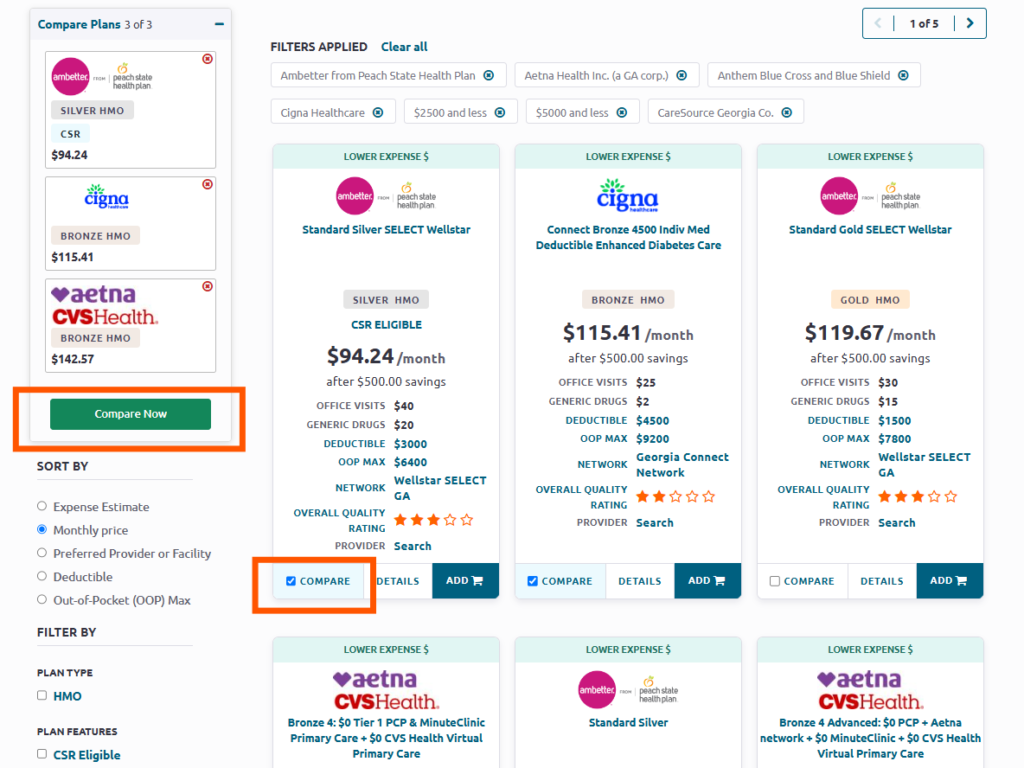

Plans are categorized as Bronze, Silver, Gold, and Platinum, each with varying levels of coverage and cost-sharing.

Comparing premiums, deductibles, and network coverage is essential to finding the right fit.

All Marketplace plans include Essential Health Benefits (EHBs), ensuring comprehensive coverage.

Enrolling in health insurance in Georgia if you’re self-employed involves several pathways:

- Georgia Access: This is the state-based marketplace offering a range of plans and potential subsidies based on your income.

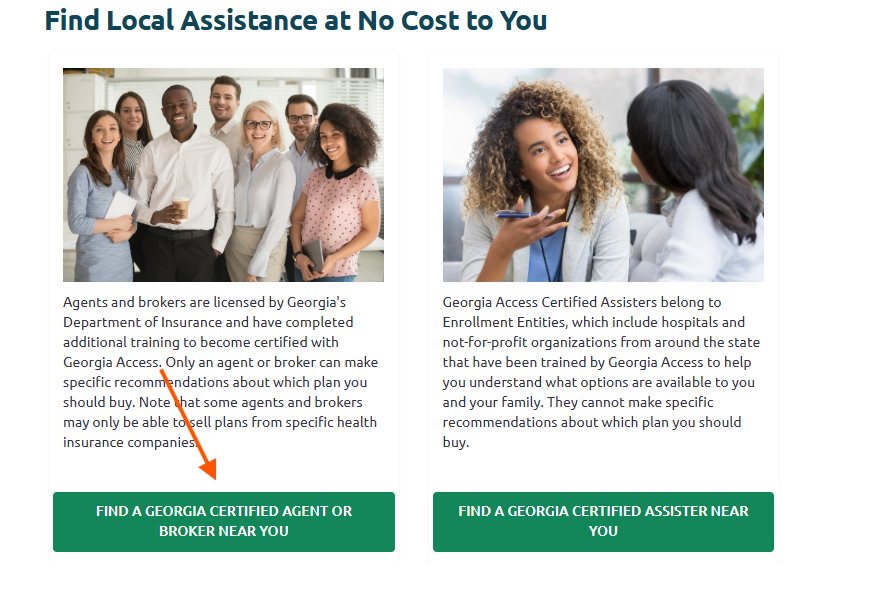

- ACA Certified Broker: Affordable Care Act certified agents and brokers have access to the same plans available on Georgia Access and can provide personalized guidance at no additional cost.

As a licensed Georgia Access partner my team offers free assistance to help you enroll in the best health insurance for your needs and budget.

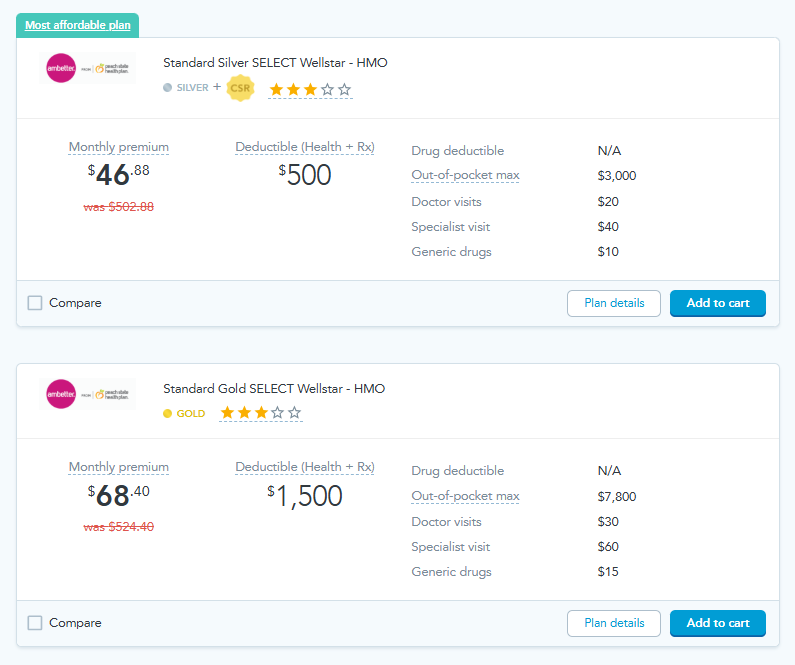

Bronze, Silver, Gold & Platinum Plans

Affordable Care Act (ACA) Marketplace plans are categorized into metal tiers – Bronze, Silver, and Gold – which represent varying levels of coverage and cost-sharing.

- Bronze Plans: These plans typically offer the lowest monthly premiums, making them attractive for budget-conscious individuals. However, they also come with the highest out-of-pocket costs, meaning you’ll pay more for deductibles, copayments, and coinsurance when you receive care.

- Silver Plans: Silver plans strike a balance between premiums and out-of-pocket costs. They often provide a good middle ground, making them a popular choice for many.

- Gold Plans: Gold plans feature the highest monthly premiums but the lowest out-of-pocket costs. This means you’ll pay less when you receive care, making them suitable for those who anticipate frequent medical needs.

In some states, Platinum plans are available.

These plans offer the most comprehensive coverage and the lowest out-of-pocket costs, but also come with the highest premiums.

Understanding these tiers helps you choose a plan that aligns with your budget and healthcare needs.

Deductibles, Cost Sharing & Out of Pocket Maximum

Understanding how these costs work is one of the most important steps for managing your healthcare expenses.

Deductibles are the amount you pay before insurance kicks in, coinsurance is the percentage you pay for covered services, and the out-of-pocket maximum is the most you’ll pay in a year.

Deductible

Knowing how deductibles work is key to managing healthcare costs.

It is the amount you’re required to pay before your insurance coverage kicks in. If you have car insurance you know how this works.

Health insurance plans have different deductibles to meet different needs and budgets.

Generally, higher deductibles result in lower monthly premiums and vice versa.

So, a healthy person who doesn’t anticipate using their plan often might choose a higher deductible to get lower premiums.

Coinsurance

Coinsurance represents the cost-sharing between you and your insurance provider after you’ve met your deductible.

It’s usually expressed as a percentage.

For example, under the Affordable Care Act (ACA) plans, you will see Bronze, Silver, and Gold tiers, each with varying amounts.

- Bronze: Insurance pays approximately 60%, you pay 40%

- Silver: Insurance pays approximately 70%, you pay 30%

- Gold: Insurance pays approximately 80%, you pay 20%

With a Silver plan, for instance, the insurer covers 70% of eligible medical expenses, while you’re responsible for the remaining 30%.

The good news is there’s a limit to what you’re responsible for.

Out-of-Pocket Maximum

ACA plans include an annual out-of-pocket maximum, which limits the total amount you’ll pay for covered services in a given year, providing financial protection.

Other than your monthly premium, anything you pay throughout the year goes toward your maximum OOP.

This includes your deductible, copays, and coinsurance.

So, if your plan has an OOP max of $2,500, the insurance company will pay 100% of your costs for the remainder of the year — minus your monthly premium of course.

When Can I Apply for Health Insurance in Georgia as Self-Employed

If you’re self-employed in Georgia, you can get health coverage through Georgia Access, the state’s new health insurance marketplace.

The best time to apply for health insurance is during the Open Enrollment Period (OEP), which typically runs from November 1 to January 15 each year.

Enrolling during this period ensures you have coverage for the following year.

However, if you experience a Qualifying Life Event (QLE) — an income change, getting married, or moving to a new area for example, you may be eligible for a Special Enrollment Period (SEP).

An SEP allows you to apply for health insurance outside of the standard enrollment window.

What’s the Best Health Insurance in Georgia for Self-Employed People?

We get this question everyday! The reality is there is no “one size fits all” when it comes to the best health insurance for self-employed.

Finding the “best” plan is subjective and depends on your specific needs. Here’s how to make an informed decision:

Are you relatively healthy, looking for basic preventative care and protection in the event of an emergency?

Or are you managing a chronic disease like diabetes that requires certain medications or specialists?

Your answers will guide your selection of plan tiers and coverage levels.

Consider your budget, too.

High-deductible plans offer lower premiums but require greater out-of-pocket expenses before coverage kicks in.

Lower-deductible plans provide more immediate coverage at a higher monthly cost.

When in doubt, you can get free assistance from a GA Access broker (like us) anytime!

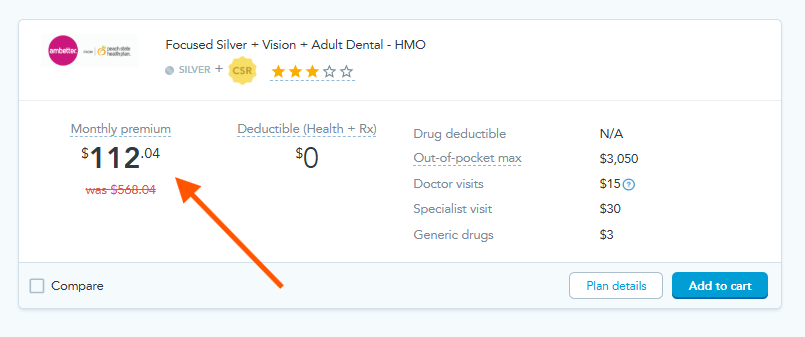

Most Affordable: Ambetter

Ideal for budget-conscious individuals, Ambetter offers competitive premiums and bundled dental/vision options.

For illustration. Plans & prices will vary. Check your ZIP Code >>

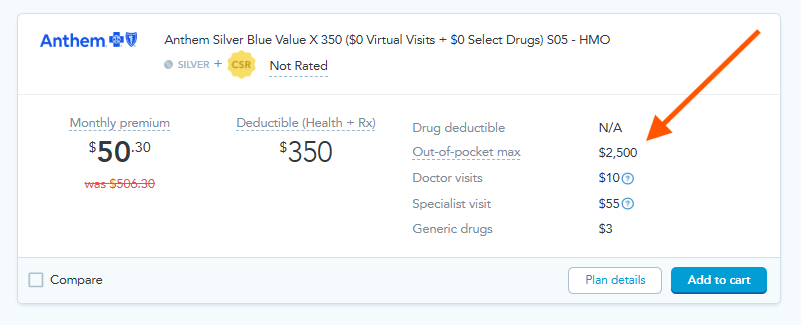

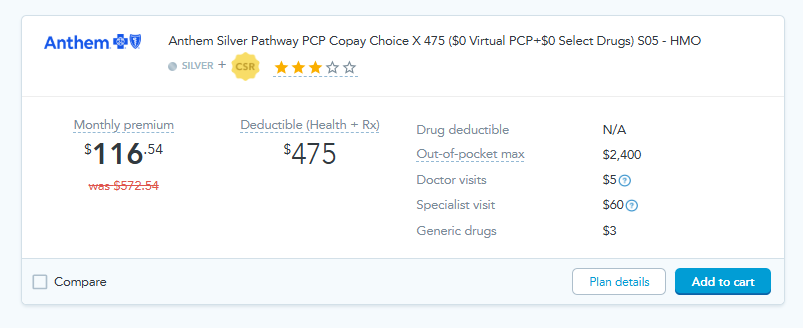

Best Network: Anthem

Anthem provides extensive provider access and comprehensive coverage, widely accepted.

For illustration. Plans & prices will vary. Check your ZIP Code >>

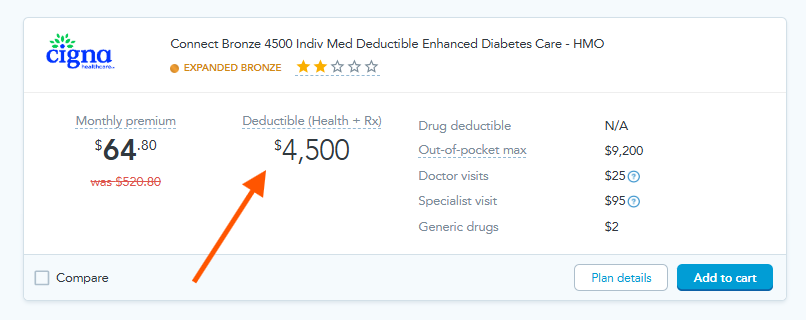

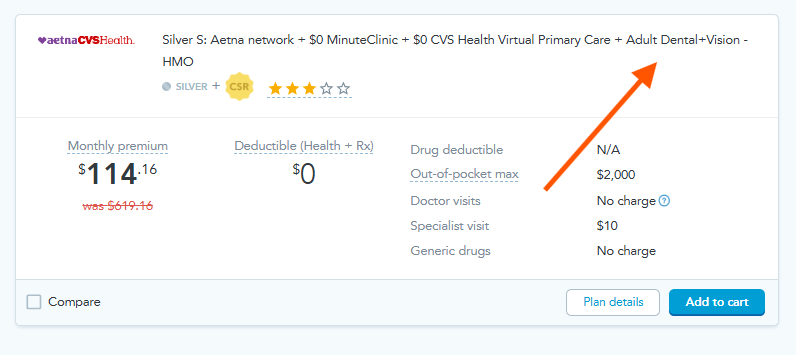

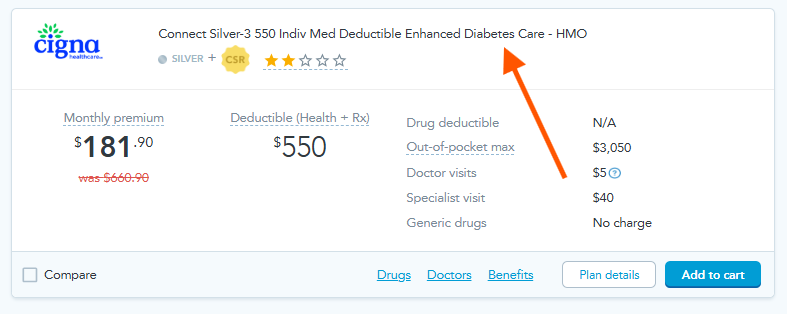

Best Overall (Tie): Aetna & Cigna

Aetna offers a balanced approach with robust coverage, a broad network, competitive pricing, and strong mental health benefits.

Large provider network, strong reputation and one of the few carriers to offer dental and vision as a bundle.

For those managing diabetes, Cigna offers specialized plans with greater savings on supplies and equipment, in addition to the benefits of the standard Cigna plans:

- $0 for preferred insulins and other diabetes medications like Basaglar, Humalog, Humalog Mix, Humulin, Farxiga, Trulicity, and Xigduo XR.

- $0 for diabetic supplies, including infusion pump maintenance, infusion sets, and skin preparation supplies.

- $0 for diabetes-related equipment, such as Dexcom G6 Receivers, Sensors, and Transmitters; FreeStyle Libre Readers and Sensors; and One Touch glucose meters.

- $0 for additional plan benefits like nutritional counseling and routine diabetic foot care

For illustration. Plans & prices will vary. Check your ZIP Code >>

Save on Georgia Health Insurance if You’re Self-Employed

As a self-employed individual, you can take steps to maximize affordability. Explore premium tax credits through Georgia Access, which can significantly reduce your monthly costs.

While health insurance may feel like a significant expense, there are ways to make it more affordable:

Most Americans use the tax credit in advance, hence “APTC” to help reduce their monthly premium now.

Keep in mind you will need to account for this credit at tax time. Always consult with a tax professional with any questions.

Marketplace employees, agents and brokers are not authorized to give tax or financial advice.

Income & Health Insurance When Self-Employed

Many of our self-employed clients experience income fluctuations throughout the year, which can make budgeting for health insurance a challenge.

The great thing about the Affordable Care Act (ACA) and Georgia Access is that if you qualify for a tax credit based on your income, it adjusts as your earnings change. Here’s how it works:

- Update Your Income Regularly

As a self-employed individual, you’re responsible for reporting any significant income changes to the marketplace.

This ensures that your Premium Tax Credit (PTC) is calculated accurately, preventing you from owing money at tax time or missing out on savings. - Income Fluctuations and Subsidies

If your income decreases mid-year, you may qualify for additional subsidies, reducing your monthly premium.

Conversely, if your income increases, updating your information helps you avoid overpayment of tax credits. - End-of-Year Reconciliation

When you file your federal taxes, the IRS will reconcile your estimated income with your actual income for the year.

Keeping your marketplace account updated minimizes the risk of surprises during tax season.

Cost of Health Insurance in Georgia for Self-Employed

The cost of health insurance for self-employed individuals in Georgia varies based on factors like age, location, income, and the type of plan you choose. Here’s what to expect:

- Average Monthly Premiums

According to Georgia Access, the average cost of marketplace health insurance for a single adult in Georgia ranges from $350 to $600 per month, depending on the plan tier (Bronze, Silver, Gold, or Platinum).

Subsidies can significantly lower this cost for those who qualify. - Out-of-Pocket Costs

Beyond premiums, consider deductibles, copayments, and coinsurance.

Bronze plans have lower premiums but higher out-of-pocket costs, while Gold and Platinum plans offer more comprehensive coverage at a higher monthly rate. - Tax Credits and Subsidies

Many self-employed individuals qualify for Premium Tax Credits through Georgia Access.

These credits reduce your monthly premium based on your income level. Cost-sharing reductions may also be available if you select a Silver plan. - Customizing Your Coverage

Georgia Access allows you to tailor your health insurance by comparing plans from leading insurers like Aetna, Cigna, Ambetter, and UnitedHealthcare.

Use their platform or consult a licensed broker to find the best value.

Tip: Always evaluate your total healthcare spending, including premiums and out-of-pocket costs, to find the most cost-effective plan for your needs.

Self-Employed Health Insurance TIPS

- Budget

Balance premiums with potential out-of-pocket costs.

High-deductible Bronze plans might work for those with minimal healthcare needs, while Silver or Gold plans are better for individuals with moderate to high medical expenses. - Provider Networks

Ensure your preferred doctors and hospitals are in-network to avoid unexpected expenses. - Prescription Drug Coverage

Check formularies to confirm your medications are included at an affordable cost. - Tax Savings

Self-employed individuals can often deduct health insurance premiums from taxable income, reducing overall costs. Consult a tax professional for guidance.

READ MORE

“Best Dental Insurance in Georgia With No Waiting Period”

Self-Employed Health Insurance vs. Small Group Health Insurance in Georgia

If you work for yourself with no employees, you’re likely shopping for individual health insurance through Georgia Access.

However, if you own a small business with employees, you may have the option to explore small group health insurance plans. Here’s a quick comparison:

- Self-Employed Health Insurance

- Ideal for individuals with no W2 employees or those running solo operations like freelancers, consultants, and gig workers.

- Available through the individual marketplace, offering a range of plans from Bronze to Platinum.

- Tax credits and subsidies may lower monthly premiums based on income.

- Small Group Health Insurance

- Requires at least two (2) W-2 employees in most cases to qualify for group plans in Georgia.

- Offers broader coverage options and potential savings, as premiums are often shared between the employer and employees.

- May provide additional benefits, such as lower premiums for the employer and employees compared to individual plans.

Key Consideration: If you’re on the fence about hiring employees to expand your business, small group health plans can be an attractive benefit to attract and retain talent.

However, for solo entrepreneurs, individual plans through Georgia Access remain the most practical option.

Free Consultation

Get help from a licensed expert with no obligation.

As an independent agency, we help individuals, families & small businesses find affordable plans and benefits in:

FL, GA, MD, NC, NJ, PA, SC, TN, TX, VA

Your privacy is our priority. We don’t share personal information or collect any payments, ensuring a safe and secure experience.

That’s BenZen.

Information is meant to be accurate and educational and not intended to be legal, medical or financial advice. Do your own research and contact a professional for help. We earn revenue from partners & advertisers. Read our disclosure for more.

Owner, BenZen Insurance. Licensed insurance broker making it easy for individuals, families and business owners to get affordable health benefits.

His background in marketing, research, insurance, and financial services gives him a unique perspective to help others plan for a secure future and improve their physical, mental, and overall well-being.