Living with diabetes can present unique challenges, including securing life insurance. While many insurers may be hesitant to cover individuals with pre-existing conditions, you can find life insurance for type 2 diabetes if you know where to look!

Diabetes can significantly impact your risk profile and, consequently, your life insurance premiums.

However, with the right information and approach, you can protect your loved ones with peace of mind.

- Underwriting Processes: Different insurers have varying underwriting standards. Some may be more accommodating of individuals with diabetes.

- Coverage Options: Explore term life insurance, which generally offers more affordable premiums compared to whole life insurance.

- Specialized Insurers: Seek out insurers that specialize in insuring individuals with pre-existing conditions.

- Accelerated Underwriting and Simplified Issue: These options may offer more flexibility for individuals with diabetes.

- Comparison Shopping: Compare quotes from multiple insurers to find the best rates and coverage.We can help.

As an independent insurance agency, we work with a variety of carriers that offer specialized products designed to meet the unique needs of individuals with diabetes.

- Banner Life (Legal & General)

- Foresters Financial

- Mutual of Omaha

Learn more about us >>

If you have diabetes and concerned about getting approved for life insurance, we can help.

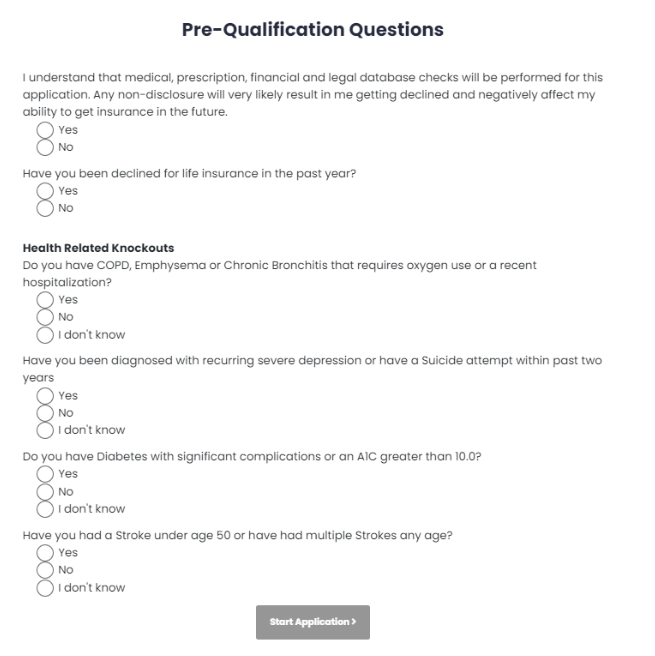

Answer these prequalifying questions to get started:

- Do you take insulin?

- What is your most recent A1C test value?

- How long have you had diabetes?

- What is your current age, height & weight

Get free expert guidance before you apply for life insurance. Contact us or schedule a phone consultation with a licensed agent weekdays, 10am-4pm EST. No obligation!

Yes. You Can Be Denied Life Insurance for Diabetes

There are many factors that can increase your risk of denial or lead to higher premiums.

Understanding these conditions before you apply is important to avoid being denied life insurance for diabetes.

Pre-existing health conditions are risky to insurance companies. While each carrier is different, many of the largest companies are not accommodating to people living with diabetes.

But this is changing.

As the number of people living with diabetes and prediabetes increases, insurers have adapted their underwriting guidelines to better serve this population.

To increase your chances of approval and potentially obtain more favorable terms, it’s essential to find insurers that specialize in covering individuals with pre-existing conditions like diabetes.

Insurers like Foresters, Banner Life & SBLI often have more flexibility in dealing with the unique challenges associated with diabetes.

You Can Be Denied for Medical Reasons

Certain health conditions and situations may lead to you being denied life insurance instantly during the application process. You should know these “knockout” questions before you apply.

This list is intended to be informational, is not all-inclusive and will vary depending on the insurance carrier you choose:

- AIDS/HIV+ status

- ALS (Amyotrophic Lateral Sclerosis)

- Alzheimer’s Disease, Dementia or significant Cognitive Impairments related to functionality

- Cancer diagnosis within the last 2 years

- Cirrhosis of the Liver

- Congestive Heart Failure

- COPD/Emphysema or Chronic Bronchitis, severe or with current nicotine use

- Cystic Fibrosis

- Diabetes uncontrolled with high A1C (>10.0)

- Muscular Dystrophy

- Heart/Cardiac Disease, multiple vessels diagnosed within the last 2 years, or any past history of current nicotine use

The Underwriting Process for Life Insurance

Underwriting is a critical step in the life insurance application process.

It involves a thorough evaluation of your risk profile to determine your eligibility, the cost of premiums, and the amount of coverage you can request.

Traditional Life Insurance Underwriting

In a traditional life insurance application, the underwriter typically requires:

- Medical exam: This may include physical examination, blood tests, and other assessments.

- Lab work: Blood tests to evaluate your overall health and identify any underlying conditions.

- Medical records: Documentation of your medical history, including previous diagnoses, treatments, and hospitalizations.

While traditional underwriting can be more time-consuming, it often provides the most favorable rates and terms if you qualify.

Life Insurance Underwriting for Diabetes

Several factors can influence your life insurance options as a person with diabetes:

- Severity of Diabetes: The severity of your diabetes, as measured by factors like A1C levels and the presence of complications, can significantly impact your risk profile and, consequently, your premiums

- Diabetes Management: How well you manage your diabetes, including your adherence to treatment plans, diet, and exercise, can influence your eligibility and the cost of premiums

- Duration of Diabetes: The length of time you have had diabetes can be a factor. Longer durations may increase your risk

- Comorbidities: If you have other health conditions in addition to diabetes, such as heart disease, high blood pressure, or obesity, your risk may be higher.

- Lifestyle Factors: Your lifestyle habits, including smoking, excessive alcohol consumption, or dangerous hobbies, can also influence your eligibility and premiums

- Age: Your age is a significant factor affecting premiums. Older individuals generally have higher premiums

- Weight: Excess weight can exacerbate diabetes and increase your overall health risks, potentially leading to higher premiums

- Coverage Amount: The amount of coverage you seek can also impact your premiums. Larger coverage amounts may require more stringent underwriting

Accelerated Underwriting vs. Simplified Issue

Two underwriting options that may be more favorable for individuals with diabetes are accelerated underwriting and simplified issue.

- Accelerated Underwriting: This involves an in-depth review of your medical history, but often with no medical exam. Offers more flexible underwriting guidelines with higher policy limits.

- Simplified Issue: This option requires less medical information and can be faster, but it may have lower coverage limits and higher premiums. It’s suitable for individuals with relatively stable health and well-controlled diabetes.

The Risks of Excessive Shopping

While it’s essential to shop around to find the best rates and coverage, excessive shopping can have unintended consequences.

The Medical Information Bureau (MIB) is a non-profit organization that collects and shares medical information about individuals who apply for life insurance.

When you apply for life insurance, your information is reported to the MIB.

Excessive shopping can lead to multiple inquiries on your MIB report, which may raise red flags for insurers. This could result in higher premiums or even denials.

- Limit inquiries: Try to keep the number of applications you submit within a reasonable timeframe.

- Be honest and accurate: Provide truthful information on all applications. Assume the insurance company can verify your answers!

- Consider pre-qualification: Some insurers offer pre-qualification options that allow you to assess your eligibility without affecting your MIB report.

- Work with an insurance agent: A knowledgeable agent can help you navigate the insurance market and find suitable options without excessive shopping.

How to Compare Life Insurance for Type 2 Diabetics

The best life insurance for diabetics depends on your individual needs and circumstances.

Some companies offer specialized programs for individuals with diabetes, while others may have more flexible underwriting guidelines. Some tips:

- Manage your condition: Good blood sugar control can help you qualify for lower premiums.

- Consider term life insurance: Term life insurance is often more affordable for individuals with health conditions.

- Shop around: Compare free quotes from different companies and get familiar with pricing.

How Much Does Life Insurance Cost?

The cost of life insurance for diabetics can vary significantly. However, you may be able to find affordable options by shopping around and comparing quotes from different companies.

For illustration only. Your rates will vary:

Example 1 – Male, nonsmoker, age 40

- 30-year term life, $100,000

- no insulin

- A1C = 9.0

- duration = 5 years

- height = 5′ 10″

- weight = 250

Premium: $40-$50 a month

Example 2 – Female, nonsmoker, age 35

- 30-year term life, $200,000

- insulin

- A1C = 8.0

- duration = 10 years

- height = 5′ 6″

- weight = 180

Premium: $80-$95 a month

Example 3 – Male, nonsmoker, age 50

- 20-year term life, $300,000

- no insulin

- A1C = 7.5

- duration = 5 years

- height = 5′ 10″

- weight = 200

Premium: $150-$200 a month

Get free expert guidance before you apply for life insurance. Contact us or schedule a phone consultation with a licensed agent weekdays, 10am-4pm EST. No obligation!

If You’ve Been Denied Life Insurance for Diabetes

If you’ve been denied life insurance due to diabetes, consider waiting a year or two before reapplying.

During this time, focus on addressing any underlying health issues that may be contributing to your risk profile.

- A1C Levels: Maintain well-controlled A1C levels to demonstrate effective diabetes management.

- Medication: Adhere to your prescribed medication regimen and consult with your healthcare provider regularly to ensure optimal treatment

- Weight Management: Strive for a healthy BMI through balanced diet and exercise. A healthy weight can significantly improve your overall health and reduce your risk of complications

- Cholesterol Control: Maintain healthy cholesterol levels to reduce your risk of heart disease, a common complication of diabetes

- Blood Pressure Management: Keep your blood pressure under control. High blood pressure can increase your risk of diabetes-related complications

Steps You Can Take

- Get a copy of your MIB Consumer File – If you’ve applied for life or disability insurance within the last 7 years you should have a file at MIB.

This report (similar to a credit report) contains much of the information insurance companies use to verify your information. It may contain your health history, medications and the results of your previous applications.

Note: Insurance companies know if you’ve applied elsewhere. Be consistent with your answers! - Employers often offer group life insurance with discounted premiums. Check with your employer to determine if a group policy is available. For the most part, your health is not a factor.

- Guaranteed-issue whole life insurance is a type of life insurance that doesn’t require you to undergo a medical exam or complete a health questionnaire.

It’s often the recommended life insurance for serious health conditions, patients and others when they don’t qualify for traditional life insurance.

Speak With A Licensed Agent

We hope this post has provided some insight as to what medical conditions can disqualify or deny you from life insurance.

During your search, there may be a time when consulting with an agent becomes necessary.

Life insurance depends on many risk factors like health, finances, credit score, lifestyle and even your driving record.

If you have questions contact us before you dive into an application.

There is no cost or obligation and it can save you time, money and the possibility of being denied coverage!